The Hospital Rake

Or: How Indian Healthcare Became the World's Most Profitable Misery Machine

The definitive field manual for the ₹17 trillion revolution that will upend how 1.4 billion people live and die.

Part I: The Body in the Morgue

There’s a business model that gets pitched in private equity meetings that sounds, on paper, like the most beautiful thing in the world. The recurring revenue is locked-in, the customers have zero bargaining power, the total addressable market is literally everyone, and the physical infrastructure creates a nearly impenetrable moat. The EBITDA margins are north of 25%. Return on capital employed is magnificent. It is a multi-decade compounding machine.

This business is, of course, a quiet, ongoing horror story. The business is Indian private hospitals.

Let me tell you how it works. Not from the glossy investor presentation, but from the morgue.

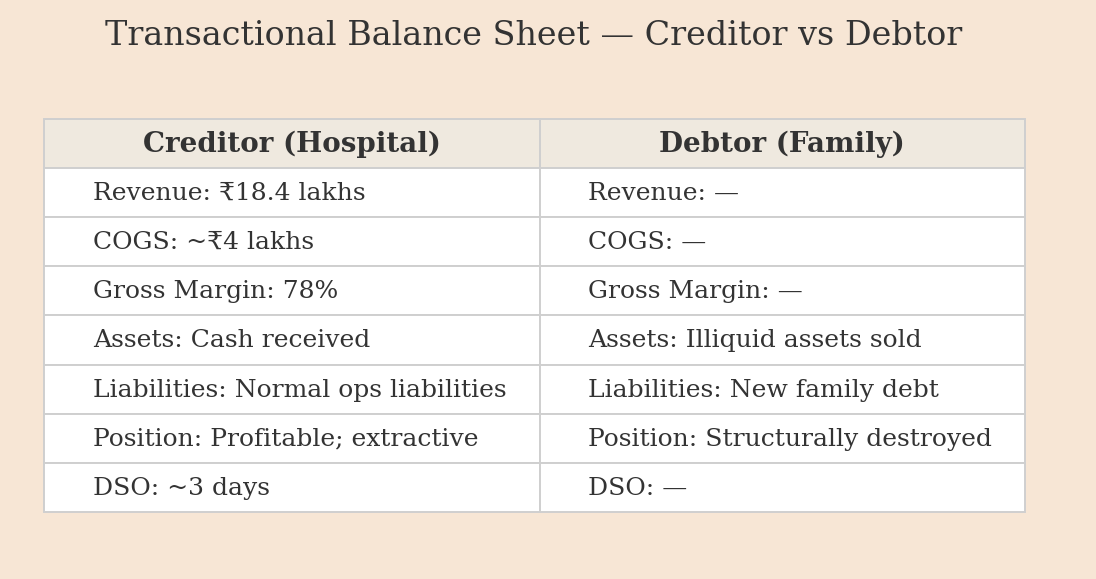

The Transaction

Let’s diagram a simple, commonplace transaction in the Indian healthcare market. You have two parties: a Creditor (a mid-sized private hospital in Koramangala, nice website, 4.2 Google rating) and a Debtor (Rajesh Kumar’s family, with a net worth composed primarily of illiquid, generational assets).

The inciting event occurs at 3 AM. A medical emergency, a heart attack, triggers a non-negotiable extension of credit. The Creditor provides six hours of services, including an angioplasty and a stent or two. The specifics are fuzzy. The services, unfortunately, are unsuccessful. At 11 AM, the Debtor’s primary asset-holder, his father, passes away on the operating table.

This is where the transaction gets interesting.

The Creditor presents an invoice for ₹18,40,000 (roughly $22,000). The Debtor’s annual household cash flow is approximately ₹6 lakhs. The invoice, therefore, represents more than 3x their gross annual income. A liquidity crisis is immediate.

The Debtor attempts to restructure the debt.

He proposes a term loan structure (installments). The Creditor, preferring lump-sum payments, says no.

He requests a haircut on the principal, questioning certain, let’s say, discretionary line items like “Miscellaneous surgical supplies: ₹3,42,000.” The Creditor, citing internal policy, says no.

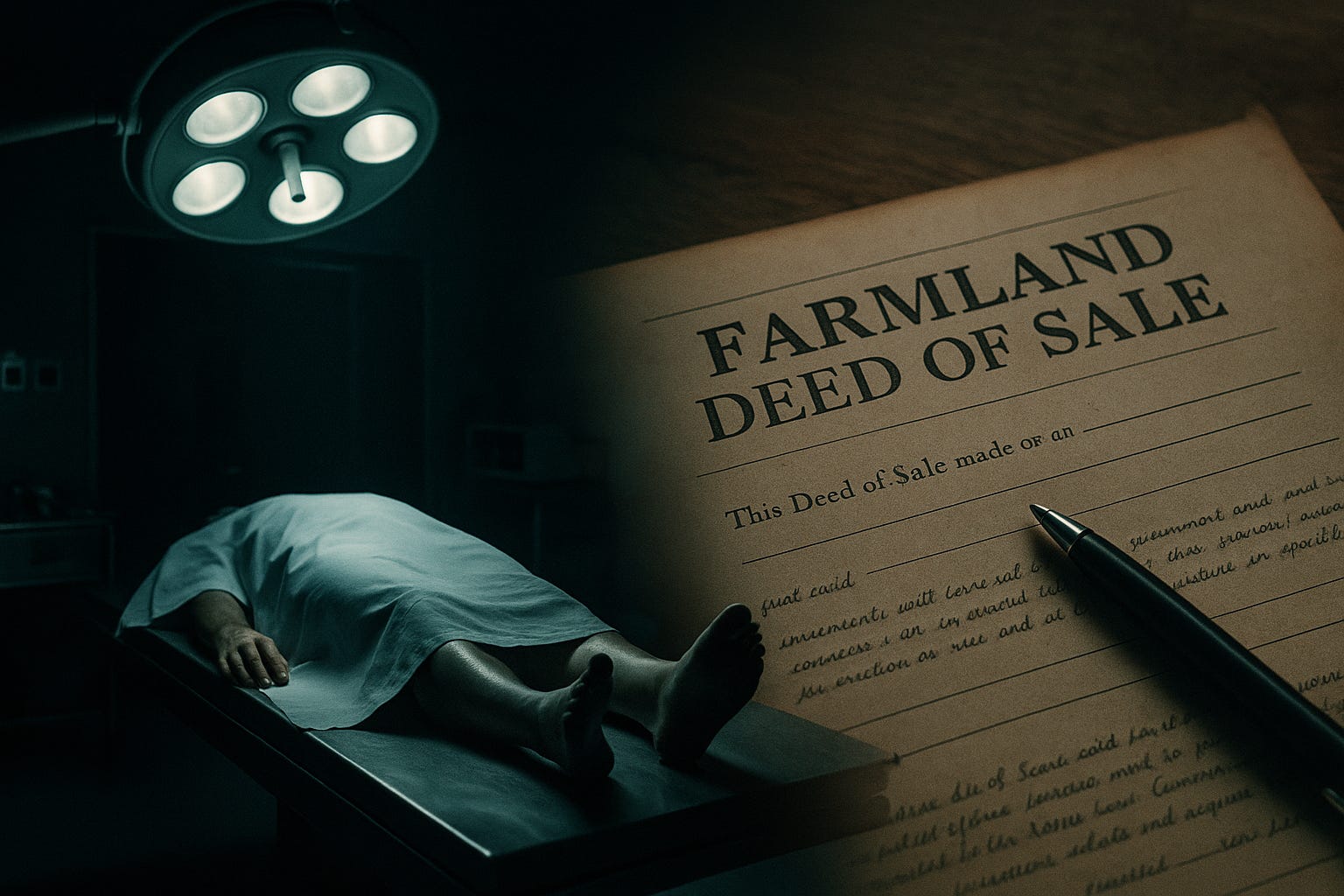

Now we arrive at the crucial leverage point. The Debtor asks to take possession of an asset currently in the Creditor’s custody: his father’s body. The Creditor, in a move of tactical genius, declines to release the asset until the debt is settled in full. The body has been converted into collateral. The hospital has effectively placed a lien on the deceased.¹

For the next seventy-two hours, the morgue functions as a high-stakes escrow account. This forces a series of emergency liquidity events on the Debtor’s side. Ancestral farmland is sold in a fire sale for ₹12 lakhs. An uncle initiates a loan against his Provident Fund for ₹4 lakhs. A brother-in-law liquidates a mutual fund portfolio for the remaining ₹2 lakhs.

On the fourth day, the Debtor settles the account. On the fifth day, the Creditor releases the collateral. The funeral is held.

Let’s analyze this transaction from both sides of the ledger:

Here is the thing that should make you want to close your laptop and stare into the void: This is not an operational failure or a moral lapse by a rogue employee. This is not a scandal. This is the business model functioning with perfect, ruthless efficiency. The 78% margin is the model. The collateralized body is the collection strategy.

Welcome to Indian healthcare. It’s a beautiful business.

The ₹39 Trillion Arbitrage

Zoom out from that one micro-transaction to the system’s macro balance sheet.

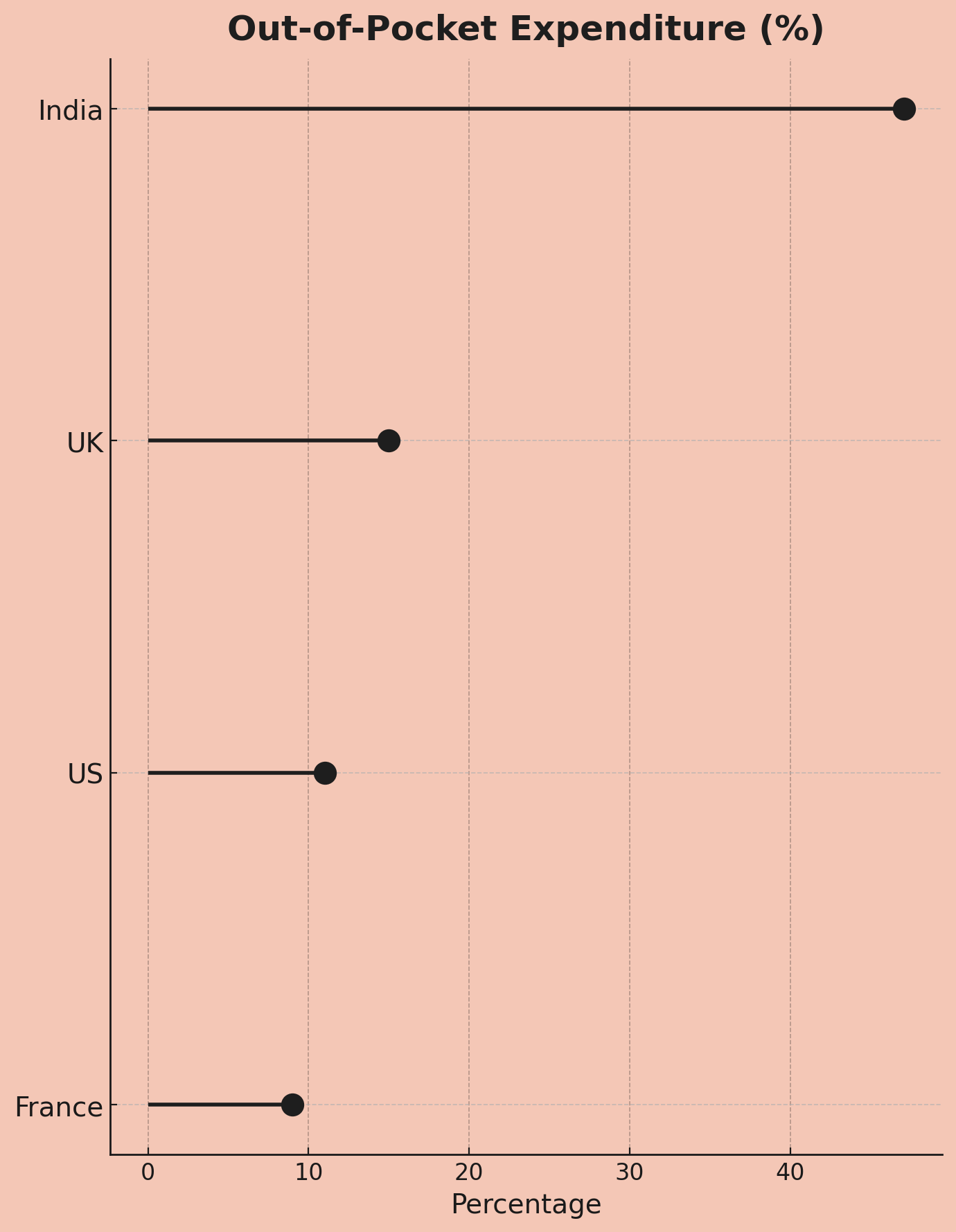

In India, the healthcare industry is funded, to the tune of 47.1%, by emergency capital calls on its customers. This is called Out-of-Pocket Expenditure (OOPE), and it means the system’s revenue is primarily sourced from whatever savings, farmland, or gold a family can liquidate at a moment of extreme duress.

This number is not just high; it’s a structural anomaly. It’s the kind of outlier that suggests you’ve found a mispriced asset. For comparison, the OOPE figures in other, more boring markets are:

The World Health Organization has a dry, technical term for the output of this model: “catastrophic health expenditure.” In India, this isn’t a rounding error; it’s a predictable, industrial-scale process. Between 32 and 39 million people see their net worth drop below the poverty line each year due to medical bills.

That is the entire population of Canada, liquidated, on an annual basis.

Now, let’s open up the annual reports of the system’s primary beneficiaries: the large hospital chains like Apollo, Fortis, and Max. They are printing 23-25% EBITDA margins. They are private equity darlings. They are, by any rational measure, absolute rocket ships.

So here is the central arbitrage of the Indian healthcare economy: How can a single system be a world-class engine for generating investor alpha and a world-class engine for generating mass poverty, at the exact same time?

The answer, of course, is that it’s not an arbitrage. It’s a direct conversion. One is simply the raw material for the other.

The 25% EBITDA margin is the balance sheet of the 39 million people who were impoverished to create it. The compounding cash flows that investors find so attractive are a clean, dollar-for-dollar ledger of the wealth extracted from millions of households at their most vulnerable. The family’s destroyed future is an externality that doesn’t require disclosure. There is, as of yet, no accounting standard for systemic misery.

To understand the architecture of this perfectly tuned machine, you have to find its source code. You have to find the Original Sin.

Part II: The Original Sin (Or: How Fee-for-Service Became Healthcare’s Flawed Operating System)

The Setup: 1991

Like most well-designed financial disasters, this one began in 1991 with the best of intentions.

India liberalized its economy. The old “License Raj” was dismantled. Capital began to flow. It was, for most sectors, glorious. But in the government’s haste to unshackle the markets, it effectively exited the healthcare business. Public health spending collapsed to a globally insignificant ~1% of GDP. This created a structurally vacant market, a perfect greenfield opportunity. The government’s message was clear: “This is a private sector problem now.”

Capital, which loves nothing more than a vacuum, poured in. A new industry of corporate hospitals was born.

And here, at the moment of creation, the original sin was committed. This new industry needed an operating system, a payment model. It adopted the only one it knew: Fee-for-Service (FFS).

FFS: A Perfectly Perverse Software

Fee-for-Service is a piece of software with one simple, elegant, and deeply perverse directive: maximize Gross Billable Events Per Patient. For every action, a test, a consultation, an incision, the provider logs a transaction and collects a fee.

In theory, this aligns payment with work done. In practice, it creates an incentive structure of almost breathtaking perversity. The system’s KPI is not “patient wellness” or “positive health outcomes.” It is “activity.” The business thrives not on health, but on sickness, and specifically, on the treatment of sickness.

More tests? More revenue.

More procedures? More revenue.

Longer stays? More revenue.

That surgery you might not need? Definitely more revenue.

You might say, “But doctors have ethics!” And they do. But they also have compensation plans. And this is where the software truly shines.

The Principal-Agent Problem, on Steroids

A hospital’s orthopedic surgeons, for instance, are often structured less like doctors and more like commission-based sales agents. They might receive 30-40% of the revenue from every surgery they perform. ²

Let’s model the choice architecture. A patient presents with knee pain.

Option A: Prescribe physical therapy. Revenue: ₹20,000. Surgeon’s Commission: ₹0.

Option B: Recommend a knee replacement. Revenue: ₹5 lakh. Surgeon’s Commission: ₹1.5-2 lakh.

This is not a story about rogue agents but about a perfectly designed principal-agent structure. The hospital (the principal) has designed a contract that incentivizes its agent (the doctor) to maximize the sale of its highest-margin products (surgeries). The agent, acting rationally, complies.

The economists call this “supplier-induced demand.” You might call it a nightmare.

It gets worse. The system has also optimized its pricing engine.

The Estimate Desk

The Estimate Desk: Dynamic Yield Management for Human Suffering

My favorite feature of this model has a certain cartoonish supervillain elegance. Many hospitals operate an “estimate desk,” which is a polite term for a bespoke price discovery unit that operates at the point of maximum emotional leverage. When a patient arrives, typically in an emergency with zero bargaining power, the desk provides an ‘estimate’.

This estimate is not a function of the medical procedure alone. It is dynamically priced based on real-time data signals of the customer’s ability to pay.

Wearing a Rolex? Estimate ↑

Arrived in Mercedes? Estimate ↑

Mentioned insurance? Estimate ↑↑ (hospital knows insurer will negotiate, so start high)

Address in wealthy neighborhood? Estimate ↑

This is textbook price discrimination, the kind of yield management airlines use for seats. Except the variable isn’t your travel flexibility; it’s your desperation to see a loved one survive.

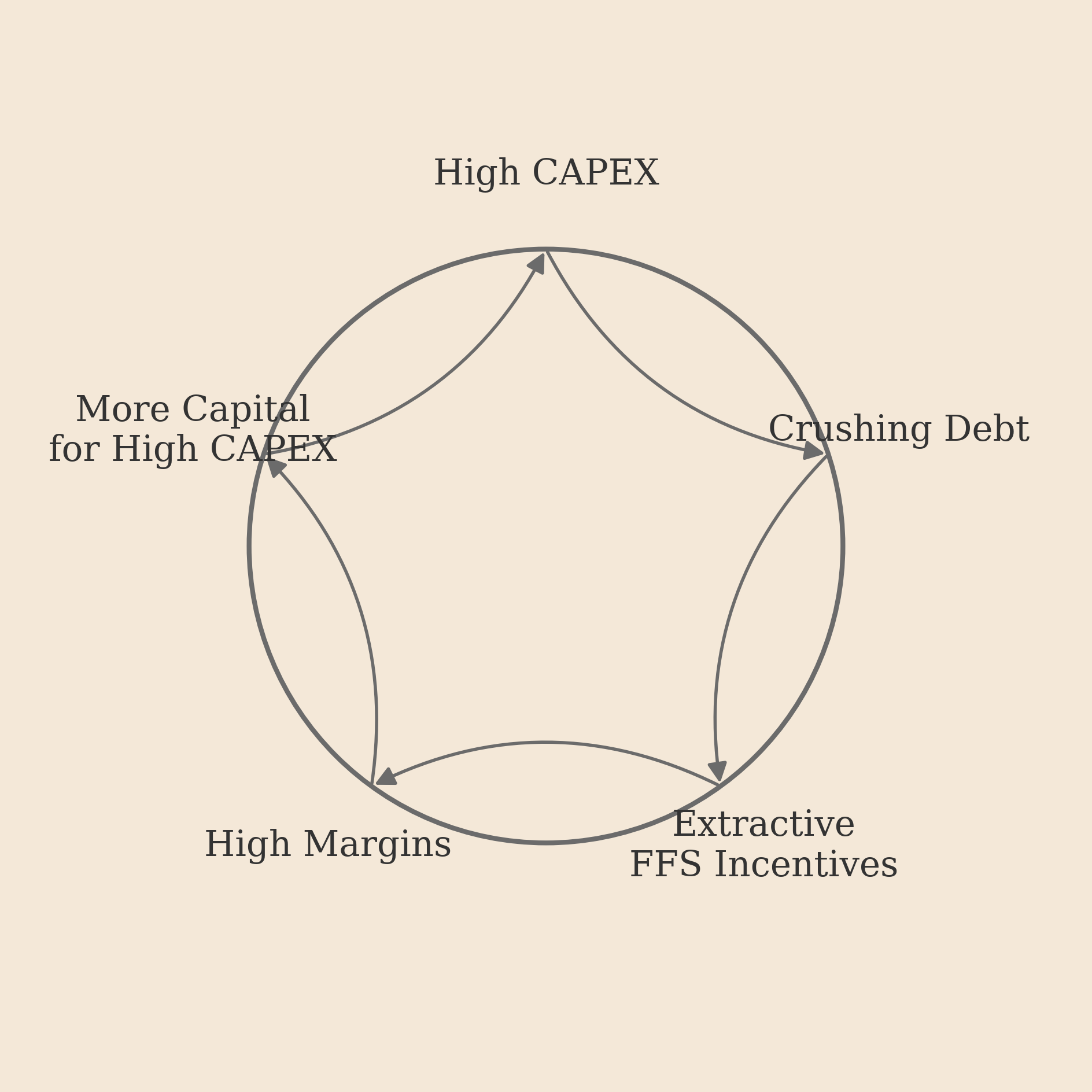

The CAPEX-Incentive Doom Loop

This extractive software runs on hardware whose economics make the whole system inescapable. Building a hospital in a place like Gurgaon is a monster of a financial problem.

Your cost structure:

Land acquisition: ₹800 crores (~$95M)

Construction: ₹500 crores (~$60M)

Equipment: ₹200 crores (~$25M)

Total Day Zero cost: ₹1,500 crores ($180M) before you’ve treated a single patient.

This is largely debt-financed. Your annual debt service, the interest alone, is a cool ₹120–150 crores. That obligation starts on Day 1. Your occupancy rate does not. The relentless pressure of that debt service dictates every operational decision. You must maximize revenue per patient. You must incentivize high-margin procedures. You must set aggressive collection targets.

The hospital isn’t evil. It is simply executing the mandate of its own balance sheet.

This creates a self-reinforcing death spiral: the CAPEX-Incentive Doom Loop.

High Capital Costs create crushing debt.

Crushing Debt demands aggressive revenue targets.

Revenue Targets are met through the FFS incentive software.

FFS Incentives destroy patient finances, but generate the margins and cash flow to...

Attract more capital to build more high-CAPEX hospitals, strengthening the loop.

You cannot fix the incentive problem (the FFS software) without solving the economic problem (the CAPEX hardware). They are one integrated system.

From an investor’s perspective, it’s a business model of exquisite, horrifying beauty. The high out-of-pocket payments mean immediate cash flow with minimal receivables. The massive CAPEX creates an impenetrable moat. The customer has zero pricing power. It’s a machine that turns human desperation into compounding returns.

And for thirty years, it has been humming along perfectly.

Until now.

Part III: The Insurgents (Or: Two Founders Try to Break the Loop from Opposite Directions)

Sometime around 2020, the Indian healthcare doom loop became so obviously, painfully broken that capital began to fund two distinct, almost philosophically opposed, attempts to dismantle it.

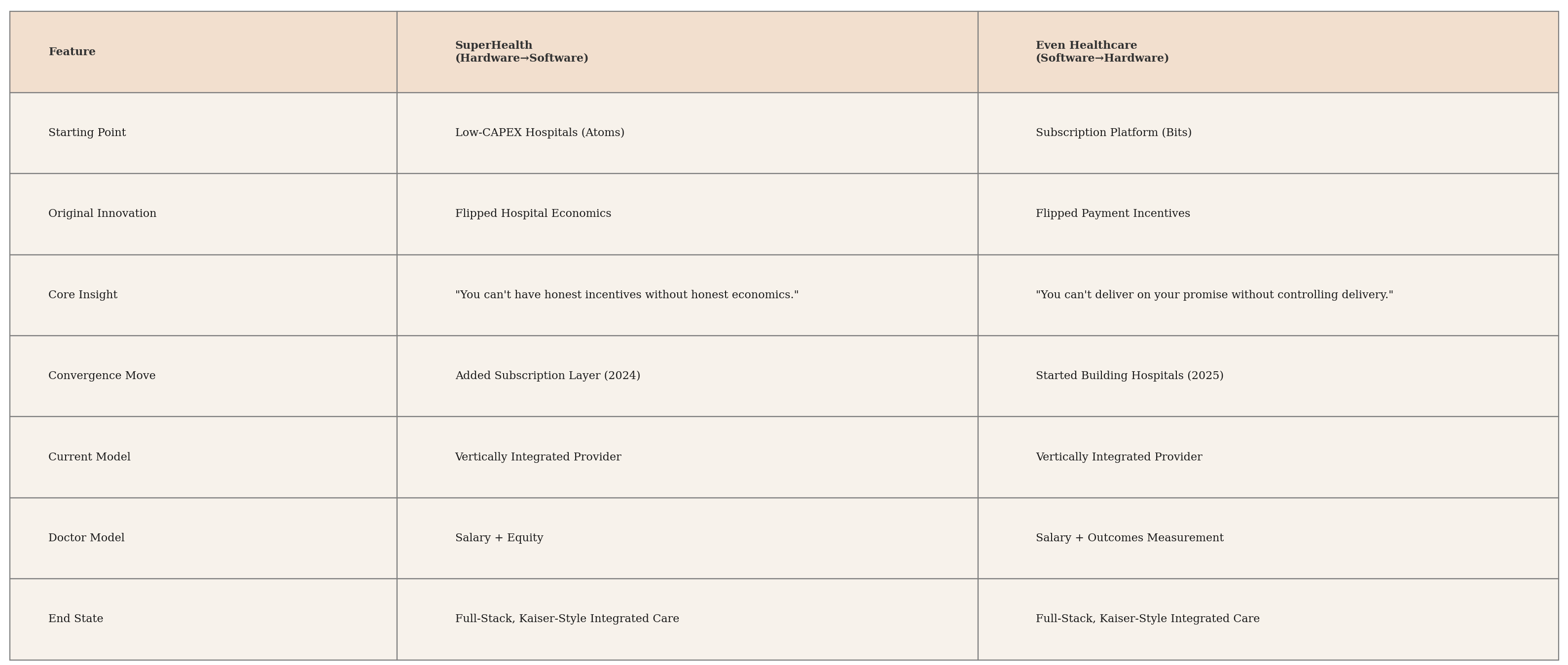

Thesis A: The Hardware Fix (SuperHealth). The core problem is economic. The crushing weight of hospital CAPEX is the original sin that forces the entire system into an extractive, FFS model. If you solve the balance sheet, you can afford to run honest software.

Thesis B: The Software Fix (Even Healthcare). The core problem is incentives. The Fee-for-Service operating system is fundamentally corrupt. If you replace the OS with a new one that aligns incentives, the hardware will be forced to adapt or die.

What followed is one of the most fascinating natural experiments in modern business: two brilliant teams attacking the same mountain from opposite faces, only to find themselves converging on the exact same peak.

SuperHealth: The CAPEX Flip

Varun Dubey, SuperHealth’s founder, came from inside the machine (Apollo Hospitals) and then learned about asset-light scaling at a canonical Indian startup (Ola). His insight was simple: what if you applied the Ola model to hospitals? Not by having freelance surgeons, but by unbundling the hospital from its most expensive, illiquid asset: the real estate.

Innovation #1: Lease, Don’t Buy

Instead of building a ₹1,500 crore glass-and-steel temple to medicine, SuperHealth finds the carcasses of the retail apocalypse, defunct Big Bazaars, empty malls, and leases them. They can stand up a fully functional, 50-bed hospital in 125 days.

The financial arbitrage is stunning:

Legacy Model CAPEX/Bed: ₹2 crores

SuperHealth CAPEX/Bed: ₹70 lakhs

This 65% reduction in capital cost is the key that unlocks everything else. It breaks the first link in the doom loop.

Really clever part: By building smaller (50 beds vs 500), SuperHealth can be hyperlocal. Building hospitals like Starbucks, one every few kilometers. Industry builds giant fortresses. SuperHealth builds distributed mesh network.

Trade-off: Can’t do every procedure in 50-bed hospital. No major trauma. No NICU. SuperHealth focuses on secondary care, planned surgeries, diagnostics, short-stay procedures. The stuff that’s 80% of hospital revenue anyway.

But how does 50-bed hospital compete with 500-bed fortress on volume?

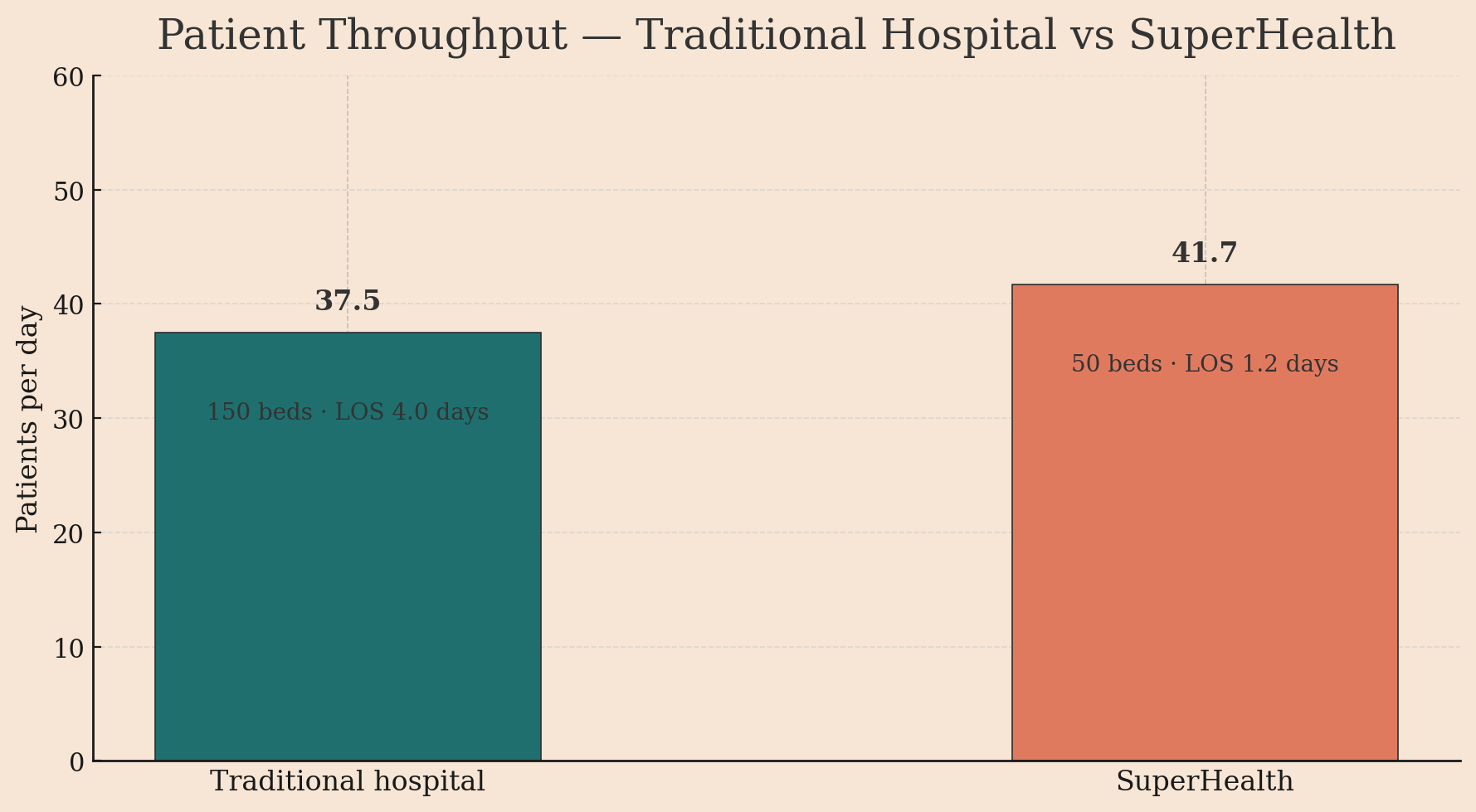

Innovation #2: The Throughput Engine

SuperHealth then rejiggers the production line. By focusing on high-volume, short-stay procedures (think cataract, hernia, basic orthopedics), they’ve unbundled the “hospital” from the “hotel.” Their Average Length of Stay (ALOS) is a blistering 1.2 days versus the industry’s 4-5 days.

Do the math: a 50-bed SuperHealth facility has a higher patient throughput (41.7 patients/day) than a 150-bed legacy hospital (37.5 patients/day).

They do this by focusing on procedures done under 24 hours:

Cataract surgery (3 hours)

Hernia repair (6 hours)

Diagnostic endoscopy (4 hours)

Most orthopedic procedures (same-day discharge)

Get in, get treated, go home to recover. Works because:

Modern anesthesia improved, you wake up faster

Surgical techniques less invasive means smaller incisions, faster healing

Most complications happen first 6 hours, after that, home is fine

By focusing on high-turnover procedures, SuperHealth processes same volume as traditional hospital with 1/3 the beds. Capital efficiency is insane.

Innovation #3: Zero Doctor Commissions

Because SuperHealth isn’t servicing a mountain of debt, it can afford to do the unthinkable: it pays doctors a salary. Plus equity. This is the magic trick. The doctor’s incentive is no longer to maximize revenue from the patient in front of them, but to maximize the long-term enterprise value of the SuperHealth brand.¹ If the brand wins, their equity prints money. If they destroy trust, they are actively lighting their own money on fire.

The “AWS for Hospitals” Play

The ambition here isn’t to build a few nice, honest hospitals. The ambition is to build 100 of them. This presents a classic scaling problem.

Historically, the quality of healthcare is artisanal. It’s a function of a specific doctor’s hands, a specific team’s chemistry, a specific facility’s culture. You can’t just Ctrl+C, Ctrl+V a great hospital. This is precisely why most large hospital chains struggle with clinical consistency; their 20th hospital is rarely as good as their first.

SuperHealth’s insight is straight out of the manufacturing and cloud computing playbooks: If you can’t scale the artisanal output, you must standardize the inputs.

The tell is their ₹2,500 crore ($300M) deal with United Imaging. This isn’t a simple procurement contract. United Imaging will now supply, install, maintain, and operate the entire radiology stack, MRIs, CTs, X-rays, across all 100 planned SuperHealth hospitals.

Let’s look at the financial engineering here, because it’s beautiful. A single high-end MRI machine is:

Expensive: A ₹15-25 crore line item on the balance sheet.

A Depreciating Asset: Obsolete in 5-7 years.

Operationally Complex: Requires specialized technicians and maintenance contracts.

Chronically Underutilized: Most hospital MRIs sit idle 50-60% of the time.

Traditionally, buying this asset is a terrible use of capital. You tie up millions in a depreciating machine that you don’t even use most of the day.

SuperHealth’s model flips this entirely. It’s a pure CAPEX-to-OPEX conversion. They turn a depreciating asset into a predictable operating expense on their P&L. United Imaging owns the machines, and SuperHealth pays a fee per scan. It’s Equipment-as-a-Service.

But that’s only the first-level genius. The second-level genius is the incentive alignment and network effects.

United Imaging ceases to be just a vendor and becomes a utilization partner. Their profit is now directly tied to maximizing the throughput of the entire SuperHealth radiology network. If one hospital’s MRI is booked solid while another’s idle, United Imaging is incentivized to help dynamically route patients between them. They can run predictive maintenance across the whole fleet, flying one technician to service ten machines in a single trip. They can arbitrage bulk pricing on spare parts.

What SuperHealth has built is a distributed hardware infrastructure with a centralized optimization layer. This is, literally, the Amazon Web Services model applied to medical hardware.

The downstream effects are even more profound. Because every hospital uses the exact same equipment, running the exact same software, the outputs are perfectly standardized. A CT scan from a SuperHealth in Bangalore is the same data object as one from Mumbai. This allows them to build a unified data lake, deploy quality-control AI across the network, and train doctors on a single, universal protocol.

This is how you solve the scaling problem. You don’t build 100 artisanal, one-off construction projects. You build a platform to deploy 100 standardized, repeatable, and infinitely optimizable healthcare factories.

Now for the other insurgent, who started from the opposite end of the stack.

Even Healthcare: The Incentive Flip

If SuperHealth’s thesis is “Fix the economics, and the incentives will follow,” Even Healthcare’s is the inverse: “Fix the incentives, and the economics will be forced to follow.”

Their founders didn’t come from the world of hospital operations; they came from insurance and managed care. They looked at the Indian healthcare machine and saw, not a CAPEX problem, but a fundamentally broken payment protocol. Their conclusion: change the way money moves, and you change everything.

Their model is a simple, radical piece of financial engineering: you pay a subscription.

That’s it. For a single, predictable monthly fee, Even effectively takes on the full liability for a person’s future health. Consultations, diagnostics, surgeries, it all moves from the customer’s P&L to Even’s.

Now, model the incentive structure. It is a perfect, 180-degree inversion of the FFS system.

Even is now, in financial terms, short your future medical bills. They have a direct, powerful incentive to keep that liability as close to zero as possible. Their entire business model moves from episodic treatment to arbitrage through prevention. The ₹500 consultation that catches pre-diabetes is a massive financial win because it prevents a future ₹5 lakh liability.

This, of course, is the classic managed care (HMO) model, the ghost protocol of Indian healthcare. It’s the model that powers giants like Kaiser Permanente in the US. The reason it never took hold in India is that it only works if you can actually control costs.

And this brings us to Even’s strategic quagmire.

The Partnership Trap

Even launched 2020 as digital-first, asset-light. Model:

You pay Even subscription

Even partners with 100+ hospitals across India

When you need care, Even directs you to partner hospital

Even pays hospital (negotiated FFS rates)

Sounds great! Even scales without building hospitals. Hospitals get patient flow. Patients get coordinated care.

Except catastrophic incentive misalignment.

Even’s goal: Keep patient healthy, minimize costs

Partner hospital’s goal: Maximize billable procedures

Every patient interaction becomes negotiation. Even’s care coordinator: “Patient needs follow-up consultation.” Hospital: “Patient needs MRI.” Even: “Protocol doesn’t call for MRI yet.” Hospital: “We’re the doctors, we decide.”

Even trying to run managed care model on top of FFS infrastructure. Like running vegan restaurant in steakhouse. Kitchen optimized for wrong menu.

Gets worse: Hospital knows Even responsible for bill, so even MORE incentive to run up costs. Insurance effect: “Someone else paying, so let’s be thorough” (read: expensive).

Even spent three years trying to make partnerships work. Built sophisticated utilization review. Hired doctors to oversee partner hospital decisions. Negotiated hard on rates.

Wasn’t enough.

Which brings us to July 2025, when Even did something that shocked entire health-tech ecosystem:

They opened their own 70-bed hospital in Bangalore.

Plans for 25 more.

The Full-Stack Pivot

Why would “software” company buy “hardware”? Because they had to.

This was the Full-Stack Pivot. It was a tacit, expensive admission of a fundamental truth: you cannot run superior software on corrupted, legacy hardware. To ensure the integrity of their incentive-aligned OS, they had to build their own vertically integrated machine. The “anti-hospital” company was becoming a hospital company, because it was the only way to build a hospital that could actually run their software.

When you own the hospital:

Doctors salaried, not commission-based

Treatment protocols standardized

Track outcomes longitudinally

Facility optimized for prevention, not procedures

No adversarial negotiation, one system

The irony is delicious: Even Healthcare, which started as “anti-hospital” company, becoming hospital company. Because hospitals aren’t the problem, incentives inside hospitals are the problem.

Even’s hospitals look different, optimized for different business model:

Facility design:

Heavy emphasis on primary care (consultation rooms, not operating theaters)

Diagnostic equipment on-site (blood work, X-rays)

Small inpatient capacity (20-30 beds for short stays)

Connected to telemedicine platform (app doctor = in-person doctor)

Clinical protocols:

Evidence-based guidelines (not “doctor’s discretion”)

Outcomes tracking (every patient’s health trajectory measured)

Preventive care emphasis (health coaching, chronic disease management)

Staffing:

Doctors paid salary, measured on clinical outcomes (patient health improvement, readmission rates)

No commission structure

Long-term employment (building relationships, not transactions)

This is what managed care looks like when you control whole stack.

Fascinating part: Even now building exactly what SuperHealth built from opposite direction.

The Great Convergence

Zoom out. What you are witnessing is a real-time A/B test of two different theories of system change, both arriving at the exact same conclusion.

SuperHealth, the hardware-first company, built its low-CAPEX hospitals and then realized that to capture long-term value and build a durable brand, it needed to own the customer relationship directly. In 2024, it bolted on a subscription software layer.

Even Healthcare, the software-first company, built its subscription model and then realized that its product was being corrupted by its reliance on a misaligned hardware layer. In 2025, it began building its own physical infrastructure.

From opposite ends of the universe, they are now building the identical thing: a recurring revenue business sitting on top of a vertically integrated physical infrastructure.

The competing theses: “Fix hardware first” vs. “Fix software first” have converged on a unified theory: in a market this broken, you cannot outsource trust.

Why? Because a partial solution is fatally compromised.

A pure-software play (Even, pre-2025) is a promise you can’t keep. You sell a subscription for “great, affordable care,” but you are contractually dependent on FFS hospitals whose entire business model is to provide “expensive, over-treated care.” The service-level agreement is fundamentally unenforceable.

A pure-hardware play (SuperHealth, pre-2024) is a product nobody trusts. You build a “low-cost hospital,” and the market reasonably assumes it’s low-cost for the wrong reasons (bad doctors, old equipment, cutting corners) because that has been the only model for 30 years.

The only way to solve this trust deficit is to control the entire value chain. To make the promise and own the delivery. From the first premium payment to the last follow-up consultation, it must all run on a single, incentive-aligned stack.

This is, of course, the blueprint for the legendary Kaiser Permanente. Kaiser is both the insurer (the payer) and the hospital system (the provider). This organisation is a piece of beautiful financial engineering. The payer side of the business is naturally short healthcare costs, while the provider side is naturally long them. By integrating them into one entity, you create a perfectly hedged system whose only remaining imperative is to reduce the underlying cost basis, which is just a financial term for “keeping people healthy.”

Finally, the system wants what you, the patient, want.

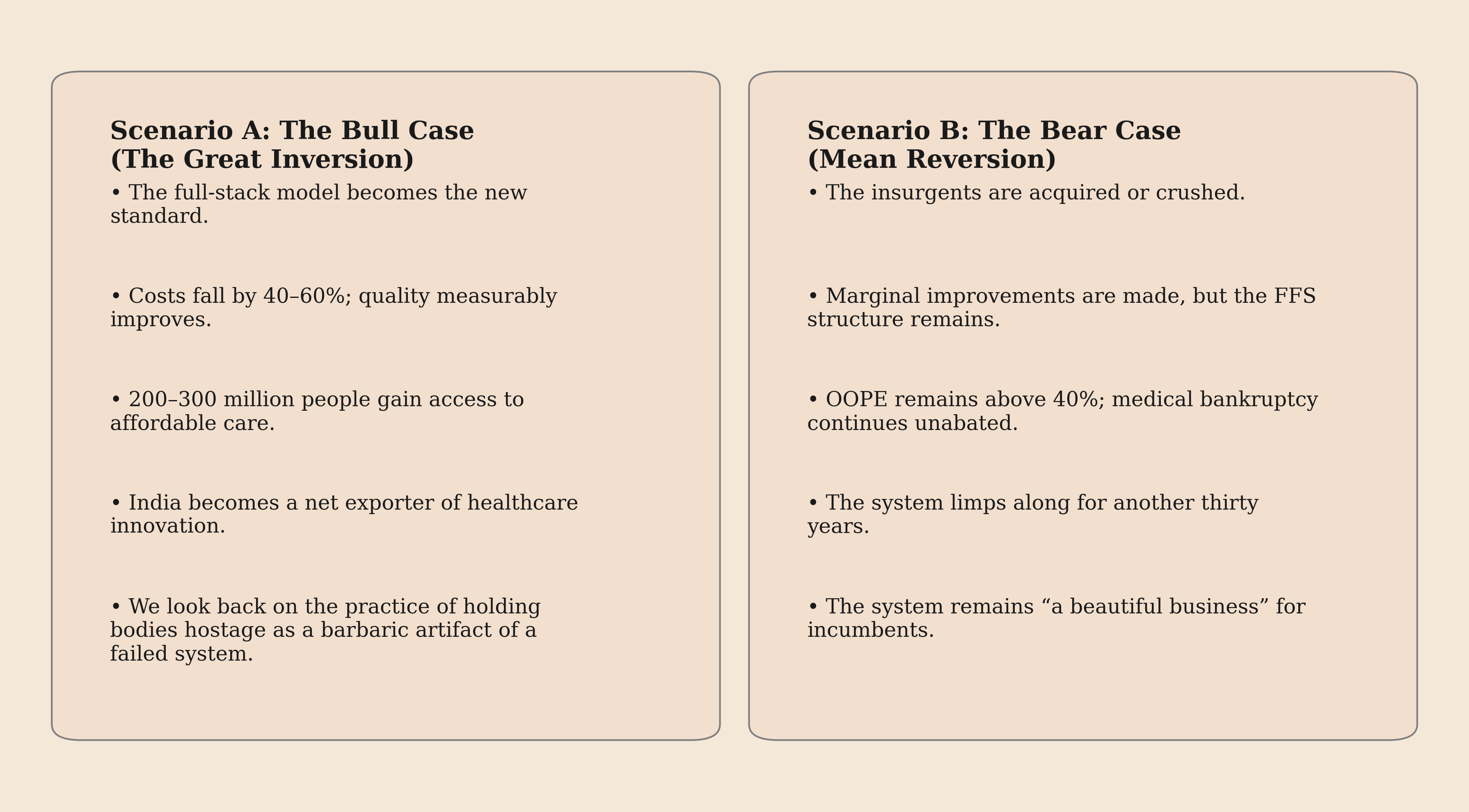

The Convergence Framework

The competitive question now is: who can traverse the stack faster? Is it easier to add a software layer to a complex physical operation, or to build a complex physical operation to support an existing software business?

My money is on the hardware-first player. Atoms are harder than bits. Building hospitals, even lean ones is a brutal game of real estate, permitting, and supply chains. Even has to learn this from scratch while SuperHealth just needs to hire product managers.

But in the end, who gets there first is less interesting than the fact that they’ve both seen the same map and are heading for the same destination.

The future of Indian healthcare is full-stack, vertically integrated, and incentive-aligned. The revolution requires nothing less.

Part IV: The Enablers

Revolutions are not spontaneous. They are the result of a specific formula: a believable precedent proves a new model is possible, new technology makes it scalable, and new regulation makes it legal.

In the 2020s, Indian healthcare finally has all three

Enabler #1: The Proof of Concept (Dr. Devi Shetty’s “Heart Factory”)

You cannot understand the current insurgency without first understanding its intellectual godfather: Dr. Devi Shetty.

In 2001, Dr. Shetty founded Narayana Hrudayalaya with a mission that sounded, to the prevailing healthcare establishment, completely insane. At a time when cardiac surgery cost ₹2-3 lakhs in India and over $100,000 in the US, he announced his intention to deliver it for ₹60,000 (then about $1,200).

He wasn’t a madman. He was simply the first person to stop thinking like a doctor running a workshop and start thinking like an industrial engineer running a factory. Instead of innovating on the surgery itself, he innovated on the production system for the surgery.

The Narayana System:

Industrialized Scale: A typical hospital might do one or two heart surgeries a day. Narayana does over thirty. This insane volume amortizes the massive fixed costs (operating theaters, equipment) across more units, drastically lowering the cost per unit. It also creates a powerful learning-curve effect: his surgeons became exceptionally good, exceptionally fast.

The Toyota Production System for Thoraxes: The operating theater was redesigned as an assembly line. Surgeons only perform the core surgical tasks. Specialized teams handle preparation, anesthesia, and closing. Operating rooms run back-to-back, minimizing downtime. Every process is standardized and checklist-driven.

Ruthless Capital Allocation: The hospital was built as a clean, functional factory, not a five-star hotel. Zero capital was wasted on marble lobbies or other non-clinical aesthetics. Every rupee was plowed into core production assets: better equipment and more capacity.

Internal Price Discrimination: Wealthier patients were charged more, creating a cross-subsidy that allowed the hospital to offer the same service to poorer patients at or below cost. (Hello, Estimate Desks!)

The results destroyed the central lie of the Indian healthcare system, that cost and quality were an inescapable trade-off.

Cost: Narayana delivered the surgery for ₹60,000-1,00,000.

Quality: Its mortality rates (1.4%) were comparable to the best hospitals in the United States (~1.2%).

Dr. Shetty proved, irrefutably, that you could have both low cost and high quality. They weren’t opposites; they were the twin outcomes of a better-designed system.

So, the obvious question: Why didn’t this model take over the world?

Narayana today is a successful chain of ~30 hospitals, but it is not the dominant force. The constraints were real:

Specialization: The “factory” model is perfectly suited for a high-volume, standardized procedure like cardiac surgery. It’s much harder to apply to the messy, unpredictable world of a multi-specialty hospital.

Culture: The system relies on an intense, almost fanatical operational discipline. Scaling that kind of human culture is notoriously difficult. ³

Capital: Even with a lean model, building 30 hospitals costs billions. Building 1,000 was, at the time, financially prohibitive.

But Narayana’s ultimate contribution wasn’t its own scale. It was that it provided the crucial proof-of-concept. It proved that the doom loop could be broken. It planted the seed of an idea that inspired an entire generation of founders, including Varun Dubey, that a better system was not just imaginable, but achievable.

Enabler #2: ABDM (The Digital Rails)

A modern healthcare system cannot be built on an analog data structure. For decades, Indian healthcare data was trapped in proprietary, disconnected silos: some digital, most in paper-stuffed filing cabinets. A patient’s medical history was effectively the property of the last hospital they visited. This wasn’t a bug but a feature of this system. It created high switching costs and massive information asymmetry, a powerful moat for incumbents.

Then, in 2021, the government began laying down a new set of public rails: the Ayushman Bharat Digital Mission (ABDM).

The vision is to do for healthcare what UPI did for payments: create a single, interoperable protocol for data exchange. Every Indian gets a unique health ID (ABHA number), which functions as a universal primary key. Every medical event: a prescription, a lab result, a discharge summary can be linked to this key, creating a longitudinal, portable health record for every citizen.

For the insurgents, this is less convenience and more a strategic weapon.

It Destroys Data Moats. With ABDM, a patient’s history is no longer held hostage by a hospital. If a customer wants to switch from an Apollo to a SuperHealth, their entire medical file can, in theory, move with them. The old system’s lock-in mechanism is vaporized.

It Creates a Common API for Health. For the first time, it becomes possible to coordinate care across a fragmented ecosystem. A specialist at Hospital A, a lab at Clinic B, and a pharmacy at Location C can all read and write to the same patient file. This interoperability is the prerequisite for building any kind of intelligent, system-wide health platform.

It Enables Competition on Outcomes. This is the killer app. Once patient data is liquid and standardized, it becomes possible to measure and compare things that were previously hidden. Patients could, in the future, see a provider’s verified readmission rates or clinical outcomes. The basis of competition shifts from marble lobbies and marketing budgets to provable quality.

Now, for the reality check. The vision is magnificent; the on-the-ground execution is, predictably, a mess. While over 620 million ABHA IDs have been created, the actual linkage of health records remains in the single digits.

The reasons are a perfect study in incentives:

Incumbent Resistance: Why would a legacy hospital voluntarily adopt a system designed to eliminate its data moat? They have every incentive to slow-roll integration and keep their data proprietary. ⁴

Technical Debt: Many smaller providers simply lack the IT infrastructure to connect to the new rails.

Data Quality: When records are uploaded, they are often incomplete or unstructured. It’s a classic “garbage in, garbage out” problem.

But here’s the crucial point: the system doesn’t have to be perfect to be revolutionary. The mere existence of these rails changes the game.

The insurgents, SuperHealth and Even, are building their entire tech stacks to be ABDM-native from Day One. They want data portability because they are betting they can win on a level playing field. They want outcomes transparency because they believe their outcomes will be better.

The incumbents are playing defense, protecting the moats of the old world. The insurgents are playing offense, building on the rails of the new one.

Enabler #3: Telemedicine Regulations (The Unlock)

For decades, telemedicine in India existed in a state of unpriced legal risk. It wasn’t explicitly illegal, but it wasn’t explicitly legal either. For any serious founder or investor, it was a “pencil’s down” problem. You simply couldn’t build a scalable business on a foundation of regulatory ambiguity.

Then came the black swan.

COVID-19 was a brutal forcing function. In March 2020, with the country in lockdown, the government’s hand was forced. In a scramble, it issued the Telemedicine Practice Guidelines, and overnight, a massive legal grey area was transformed into a clearly defined, permissible activity.

This was the regulatory unlock for the entire software-first healthcare thesis.

For a company like Even Healthcare, the subscription model is only viable if the marginal cost of a “consultation” is driven toward zero. An “unlimited” offering is economically catastrophic if each unit of consumption is a high-cost, in-person event.

Telemedicine fundamentally rewrites the cost curve of primary care.

Legacy Model: A ₹500-1,000 in-person consultation involves real estate overhead, scheduling friction, and limited doctor capacity (maybe 15-20 patients/day).

Telemedicine Model: A video consultation strips out nearly all of that overhead. It’s just the doctor’s time and a sliver of platform cost. The throughput of that same doctor can triple to 50+ consultations/day.

It effectively turns primary care from a high-touch, location-based service into a low-touch, scalable software product.

The Moral Hazard Reversal

This new, ultra-low-cost interaction enables a beautiful piece of economic jujitsu.

In traditional insurance, “moral hazard” is the enemy. When a service is free at the point of use, people tend to over-consume it, driving up costs. The entire industry is built to create friction to prevent this.

The subscription-plus-telemedicine model inverts this. It makes a feature out of the bug. When consultations are “free” and frictionless for the subscriber, they are encouraged to call at the first sign of a problem.

This “over-consumption” of cheap, early-stage care is the system’s most powerful risk-management tool. A ₹100 video call today is an incredible arbitrage against a potential ₹5 lakh hospitalization in the future. The model weaponizes the patient’s tendency to seek care, using it as a data-gathering and early-intervention mechanism.

Yes, there are still limitations: rules around the first consultation being in-person, prescription restrictions, and murky liability frameworks. But the core unlock is done.

The regulatory environment for a foundational piece of the new healthcare stack went from pending_approval to active. The software-first revolution now had a legal API to build on.

Enabler #4: The Unfinished Revolution (Insurance)

Here is the dirty secret: the Indian health insurance industry is a beautifully designed, zero-sum war. And the patient is the battlefield.

On one side, you have the hospitals, running on the Fee-for-Service (FFS) OS. Their mandate is to maximize billable events. On the other side, you have the insurance companies, whose mandate is to minimize payouts. The entire system is an adversarial negotiation over a sick person’s body. The Third-Party Administrators (TPAs) are the hired mercenaries in this war, often incentivized to deny claims. ⁵

This is not a bug. It’s the inevitable outcome of a system where the insurer reimburses the provider on an FFS basis. It is a structure of perfectly misaligned incentives.

The solution is an elegant piece of financial engineering called value-based payment, or capitation. In this model, the provider is paid a fixed fee per person, per year. They are no longer selling procedures; they are selling outcomes. They have effectively taken a long position on their patient’s health. If the patient stays healthy, the provider profits. If the patient gets sick, the provider’s margin erodes.

Finally, everyone: provider, payer, and patient is on the same side of the trade.

So why hasn’t this obviously superior model been implemented? The regulator, IRDAI, has been exploring it for years, but the system is stuck.

Incumbent Resistance: Why would a hospital chain earning 25% EBITDA margins on an FFS model voluntarily switch to a capitation model that might earn 10% by keeping people out of their beds?

Underwriting Risk: You can’t price a capitated plan without good data on future costs. India, until recently, didn’t have that data (see: ABDM).

Adverse Selection: The first people to sign up for an “all you can eat” healthcare plan are the hungriest. This risk can bankrupt a poorly designed plan.

But here’s the strategic masterstroke: Even Healthcare is not waiting for this revolution. It is becoming the revolution.

Even is not trying to sell its software to the legacy insurance companies. It is disintermediating them. By being both the payer (taking the subscription fee) and the provider (managing the care), it has created a closed-loop, fully-capitated system from scratch. It is running a live, direct-to-consumer pilot for the future of the entire industry.

If this pilot works at scale, it creates a powerful forcing function. Legacy insurers will have no choice but to copy the model, or risk becoming obsolete.

This is how true system change happens. It doesn’t come from a top-down regulatory mandate. It comes from a bottom-up insurgent who builds a new, better machine, proves the unit economics, and then drags the entire market into the future.

The timeline becomes clear:

2025-2030: The insurgents prove the D2C capitation model is viable.

2030-2033: The model is de-risked. Progressive insurers and state governments launch their own pilots.

2033-2035: The evidence is overwhelming. Regulation catches up to reality, making value-based payment the default.

2035+: The FFS war becomes a historical relic.

The revolution in insurance won’t be televised, it will be built, one subscriber at a time.

Now we need to talk about why this might all fail.

Part V: The Bear Cases (Or: Every Way This Revolution Could Collapse)

Every magnum opus needs this section. Where we steelman the opposition. Where we’re intellectually honest about what could go wrong.

Because here’s the thing: Most revolutions fail. The insurgents get crushed. The incumbents adapt just enough to survive. The system limps along for another decade.

So let’s talk about every way this could collapse.

Bear Case #1: The Trust Problem (”Cheap = Bad” Is Culturally Embedded)

Thesis: The single greatest moat protecting the incumbent hospital chains is not capital, nor regulatory capture, but a deeply embedded market heuristic: in Indian healthcare, price is the primary signal for quality.

This isn’t irrational consumer behavior; it’s a logical response to decades of operating in an information-asymmetric market. In the absence of reliable, transparent data on clinical outcomes, patients have been forced to rely on proxies. And the most powerful proxy is the price tag. The ₹30 lakh car is probably safer than the ₹10 lakh car. The five-star hotel is probably cleaner than the no-star one.

For thirty years, this has held true in healthcare. The gleaming Apollo with its marble lobby wasn’t just selling luxury by engaging in cost signaling. The conspicuous capital expenditure was a hard-to-fake signal of financial stability and, by extension, a commitment to a certain standard of clinical quality. It was a rational choice for a consumer to believe the expensive hospital was less likely to let them die.

This presents a brutal challenge for the insurgents. Their entire model is based on a positive arbitrage: they claim their lower prices are the result of superior operational efficiency and a leaner capital structure. But the market has been trained to interpret lower prices as a signal of a negative arbitrage: corner-cutting, underpaid doctors, and inferior equipment.

The Playbook to Overcome This:

This is, fundamentally, a go-to-market and brand-building problem. The insurgents aren’t just selling healthcare; they are attempting to re-educate an entire market on how to evaluate quality. Their strategy must be a multi-pronged assault on the old heuristic:

Weaponize Transparency. The only way to beat a bad signal (price) is with a better one (data). The insurgents must relentlessly publish their clinical outcomes: readmission rates, infection rates, patient satisfaction scores. They need to make their data so radically transparent that it becomes the new benchmark for the entire industry.

Manufacture a New Brand Signal. Trust is a function of time and consistency. The brand must be built on years of flawless execution. A single high-profile medical error in the early days could be an extinction-level event, as it would confirm the market’s worst fears about “cheap” healthcare.

Execute a Talent Arbitrage (and Publicize It). The most powerful signal they can generate is convincing a star surgeon from a top-tier hospital to take a pay cut to join their salaried model. This is a public declaration of belief from a credible insider, signaling that the “smart money” in the medical community is betting on the new system.

Find the Wedge Customer. They cannot win the premium customer on Day One. The ₹50 lakh/year family will continue to use price as a safety signal. The strategic wedge is the family earning ₹8-12 lakhs: they are priced out of the premium incumbents but are terrified of the quality in the lower tiers. This is the segment that is most receptive to a new value proposition.

Verdict: This is not a fatal flaw in the business model, but it is the primary go-to-market risk. It requires a brutal, multi-year grind to build a new brand from scratch. The product they are really selling is Trust-as-a-Service, and that is a hard product to scale.

Bear Case #2: The Talent Problem (You Can’t Find 10,000 Ethical Doctors)

Thesis: The insurgents’ elegant financial and operational models are irrelevant if they cannot solve the single biggest input variable: acquiring and retaining high-quality medical talent at scale in a market that has been optimized for a different compensation structure for 30 years.

This is the existential execution risk. A hospital is not its building or its balance sheet; it is the collective expertise of its doctors and nurses. If you cannot solve for the “who,” the “how” and “what” are just theoretical models on a spreadsheet.

Let’s quantify the challenge. SuperHealth’s plan for 100 hospitals requires them to recruit, train, and retain roughly 1,700 physicians and over 8,000 nurses and technicians. The fundamental problem is that the entire existing market for this talent has been conditioned by the Fee-for-Service (FFS) system. They are trying to convert a generation of commission-based free agents into salaried, equity-holding employees.

This presents four structural headwinds:

The Compensation Delta: A top orthopedic surgeon at an incumbent hospital can clear ₹1 crore/year, with a significant portion being variable, performance-based commissions. The insurgent offer is a lower cash salary (e.g., ₹50-60 lakhs) plus a pile of illiquid, high-risk startup equity. For a mid-career doctor with a mortgage, this is a tough trade.

Career Risk: The career path in legacy healthcare is linear and predictable. Joining an unproven startup is a high-variance deviation from that path.

The Adverse Selection Trap: This is the most dangerous risk. Who is most likely to be attracted to a model that doesn’t reward “sales”? It might be the doctors who were never very good at “selling” procedures in the first place. The insurgents could inadvertently be selecting for the bottom quartile of the talent pool, creating a self-fulfilling prophecy of inferior quality.

The Churn Problem: If the model fails to provide sufficient financial or professional satisfaction, it will create a revolving door. High doctor churn is a unit-economic cancer that destroys clinical consistency and brand trust.

The Human Capital Arbitrage Playbook

The insurgents cannot win a head-to-head bidding war for talent. Their entire strategy, therefore, must be to find undervalued or mispriced assets in the human capital market. They are not trying to recruit every doctor; they are trying to build a coalition of specific doctor archetypes who are systematically undervalued by the FFS machine.

Segment #1: The Uncorrupted. Target top residents straight out of medical school. They are clinically skilled but have not yet been financially anchored to the commission model. The pitch: “Practice medicine the way you were taught it was supposed to be.” Lock them in with a four-year equity vesting schedule.

Segment #2: The Burnouts. Target the successful, mid-career FFS doctors who are financially secure but morally exhausted. The product you are selling them isn’t wealth; it’s psychic income, the ability to practice medicine without the guilt of over-treatment, and a more predictable work-life balance.

Segment #3: The Diaspora. Go after the vast pool of Indian doctors trained and working in salaried systems abroad (US, UK, Gulf). Many want to return to India but are repulsed by the local FFS culture. The insurgents offer them a unique proposition: a Western-style professional environment in their home country.

Verdict: This is the single biggest bottleneck to scale. The entire thesis rests on the hypothesis that a sufficient number of high-quality doctors exist in these three segments to staff a national chain. The model’s ultimate success will not be measured in EBITDA margins, but in its doctor retention rate and Net Promoter Score. The early signals that both companies are oversubscribed with applicants are positive, but scaling the human element from dozens to thousands is where most revolutions die. The algorithm is elegant; the wetware is the variable.

Bear Case #3: The Adverse Selection & Risk-Pooling Problem

Thesis: The insurgents’ beautiful unit economics are not the product of genuine operational innovation, but of a clever risk-selection strategy. They are arbitraging the healthiest, lowest-cost segment of the patient population, and their model would collapse if forced to absorb the costs of the system’s statistically inevitable, high-cost tail.

This is the classic, brutal critique of any new entrant in a risk-based business. It’s easy to look like a genius when you only underwrite the good risks.

The accusation manifests differently for each model.

For SuperHealth: The Case Mix Accusation

SuperHealth’s operational model is a high-throughput factory for high-margin, low-volatility procedures: a cataract surgery, a hernia repair. These are the financial equivalent of investment-grade bonds: predictable, short-duration, and low-risk.

The core of the bear case is that their P&L is not built to handle the “junk bonds” of healthcare:

The trauma patient with a multi-week ICU stay.

The oncology patient requiring months of unpredictable treatment.

The diabetic with multiple comorbidities whose simple surgery cascades into a complex, high-cost event.

These are the long-tail, high-cost liabilities that sink hospital balance sheets. If SuperHealth were forced to take on a statistically normal distribution of these cases, would their lean, high-throughput model buckle? Would their 1.2-day Average Length of Stay balloon? Would their margins evaporate?

SuperHealth’s Defense: Their argument is that this isn’t cherry-picking; it’s strategic unbundling. They are not trying to be a full-service, universal hospital. They are a specialized factory. They are unbundling the predictable, high-volume “manufacturing” work of healthcare from the chaotic, bespoke “R&D” and “emergency response” work. This is a legitimate strategic defense, but it also means they are not, in fact, a replacement for the entire system, but rather an optimization layer for its most profitable component.

For Even: The Actuarial Death Spiral

Even’s vulnerability is more acute and existential. Their entire business is a capitated risk pool. They are making an actuarial bet that the premiums collected from their members will exceed the healthcare costs those members generate.

The mortal enemy of any risk pool is adverse selection. The people with the highest propensity to sign up for an “all you can eat” healthcare plan are the ones who intend to eat the most. If Even’s risk pool becomes disproportionately populated with the sickest, most expensive patients, it will enter a classic insurance death spiral: high costs force them to raise premiums, which causes the healthiest members to leave, which further concentrates the risk, which forces premiums even higher, and so on, until bankruptcy.

Even’s Defense Mechanism: They are, by necessity, an insurance company, and they must use the tools of insurance to survive.

Risk-Adjusted Pricing: They cannot offer a single flat price. They must underwrite, charging higher premiums for older members or those with pre-existing conditions.

Careful Underwriting: In the early days, they must be selective about who they allow into the pool, potentially excluding the highest-risk individuals. This, however, puts them in a tricky position: if they are too selective, they are not a healthcare solution but simply an “insurance for the healthy.”

Population-Based Acquisition: The best way to build a stable risk pool is to acquire an entire, statistically normal population at once, for example, by signing up all the employees of a large corporation. This diversifies the risk portfolio instantly.

Verdict: This is a structural and legitimate concern. The only way for the insurgents to counter this critique is with radical transparency. They must publish their data: their case mix index, the average acuity score of their patients, and a demographic comparison of their patient base to the general population. If they want to claim they are solving the healthcare problem, they have to prove they can build a profitable model that serves the sick, not just a walled garden that serves the well.

Bear Case #4: The Diseconomies of Scale

Thesis: The insurgents’ model is a beautiful, fragile jewel that only works at sub-scale. As they grow, the very forces they’ve harnessed will turn against them, and their elegant unit economics will collapse under the weight of organizational complexity and market realities. Success will be its own poison.

This is the “success disaster” scenario. The model works so well at 10 units that they raise a billion dollars to build 100, and in the process of scaling, they inadvertently become a slightly cheaper, less efficient version of the very incumbents they sought to destroy.

The decay will happen across four vectors simultaneously:

The Arbitrage Evaporation (Real Estate & Talent)

The early model is built on clever arbitrage. SuperHealth finds undervalued, distressed real estate. Both insurgents find undervalued human capital (the doctors disgusted with the FFS system). But as you scale from 10 to 100 locations, you are no longer an agile opportunist; you are a predictable, whale-sized player in the market.Real Estate: Landlords are no longer negotiating with a desperate startup; they are negotiating with the future of healthcare. Lease rates will climb. The initial 65% CAPEX advantage will start to erode.

Talent: As you hire hundreds of doctors, you saturate the niche pool of “true believers.” You are now competing for the median doctor, who is more mercenary. This will drive up salaries, shrinking the compensation gap and weakening the model’s cost advantage.

The Decay of Culture and Control (Management)

At 10 hospitals, the founder is a panopticon. They can visit every facility, know every senior doctor, and personally transmit the cultural DNA. At 100 hospitals, this is impossible. You have to insert layers of abstraction: regional VPs, district managers, a professional bureaucracy.The tight, mission-driven culture that produced the initial magic gets diluted.

Principal-agent problems multiply down the chain of command.

The organization begins to develop the very bureaucratic sclerosis it was designed to replace.⁶

The Entropy of Execution (Quality Control)

How do you ensure that Hospital #87 in Ranchi is delivering the same standard of care as the flagship in Bangalore? Without the founder’s direct oversight, and without the sharp, transactional incentive of FFS commissions, what prevents standards from slipping? How do you stop a rogue clinic manager from quietly re-introducing under-the-table incentives to boost their P&L? The system, like all complex systems, will naturally tend toward entropy. Preventing this requires a massive, ongoing investment in quality control systems that adds to the overhead and complexity the model was supposed to avoid. This is the United Airlines Risk: the company grows so fast that its operational quality collapses, and the brand becomes synonymous with the very mediocrity it disrupted.Painting a Target on Your Back (Regulation)

When you are a small, cute innovator, regulators and incumbents ignore you. When you are a rapidly scaling threat to a ₹5 trillion industry, you become Public Enemy Number One. The incumbents will not compete with you on price or quality; that’s too hard. They will compete with you in the halls of government. They will lobby for new regulations designed specifically to kill your model: minimum CAPEX requirements, scope-of-practice restrictions, new licensing hurdles. You go from being an innovator to being a target.

The Mitigation Playbook

This slide into mediocrity is not inevitable, but avoiding it requires a fanatical, almost paranoid discipline.

Scale Oversight with Technology. You cannot scale the founder, but you can scale their oversight. This means building a powerful central nervous system: an AI-driven platform that monitors clinical protocols, flags billing anomalies, and tracks outcomes across the entire network in real time.

Distribute Ownership. You have to fight bureaucracy by aligning incentives at the edge. This means giving local hospital CEOs and lead doctors significant equity, making them partners with skin in the game, not just employees in a hierarchy.

Choose Your Growth Rate Wisely. The ultimate defense is to resist the VC-fueled pressure to blitzscale at all costs. A flawlessly executed network of 30-40 hospitals is infinitely more valuable and defensible than a messy, inconsistent network of 100. This requires a strategic decision to prioritize operational integrity over market share growth.

Verdict: This is the most insidious risk, because it’s a byproduct of success. The core model is sound. The danger is that the physics of corporate gravity will inevitably pull the insurgents back down to the mean. Their greatest challenge is not disrupting the old system, but avoiding becoming it.

Bear Case #5: The Incumbent Counterattack (Apollo Launches “Apollo Honest”)

Bear Case #5: The Innovator’s Dilemma

Thesis: The insurgents are not fighting a startup; they are fighting a dormant giant. The moment their model is de-risked and proven profitable, the giant (Apollo, Fortis, etc.) will wake up, copy the playbook, and use its immense structural advantages: brand, capital, and distribution, to crush them.

This is the classic, terrifying “Innovator’s Dilemma” scenario. The insurgents do all the hard, risky work of market creation, and the incumbent, having watched and learned, swoops in for the kill.

On paper, the incumbent’s advantages are overwhelming:

Brand as a Moat: “Apollo” is a trusted, Schelling point for quality. “SuperHealth” is an unknown quantity.

Cost of Capital: A publicly traded giant can raise billions in debt at low interest rates. The insurgents have to sell expensive equity to VCs.

Distribution & Relationships: The incumbents have decades-long contracts with every major corporation and insurer. They are already embedded in the system.

The War Chest: An incumbent can subsidize a new, low-margin “Apollo Lite” venture for years, bleeding it dry with cash from its profitable core business, an option the insurgents simply don’t have.

So, what stops Apollo from launching “Apollo Honest” tomorrow and ending this revolution before it begins? The answer is that the very structure that makes them powerful also makes them inert.

The Cannibalization Mandate

The FFS model, for all its horrors, prints 25% EBITDA margins. The insurgents’ lean, honest model might print 10-15%. For a public company CEO, launching a new, lower-margin business that will directly compete with and steal customers from your primary cash cow is a structurally irrational act. Your job is to protect margins, not voluntarily compress them. Why would you introduce a product that makes your own business less profitable? ⁷The Incentive & Contractual Hairball

An incumbent like Apollo has thousands of doctors operating under commission-based contracts. This isn’t just a compensation policy; it’s the load-bearing wall of their entire human capital structure. You cannot simply flip a switch and move everyone to a salaried model. Your best, highest-producing “salesmen” would walk. Re-architecting this would require untangling a decade of principal-agent knots, a task so complex and politically fraught that it’s almost unthinkable.The Cultural OS

For forty years, Apollo’s entire corporate organism, from the CFO to the ward nurse has been optimized to answer one question: “How do we maximize Average Revenue Per Occupied Bed (ARPOB)?” SuperHealth’s culture is designed to answer, “How do we maximize patient trust and lifetime value?” These are fundamentally different operating systems. An incumbent cannot simply install a new culture like a software patch; it’s embedded in every process, every KPI, and every middle manager’s quarterly bonus.

To truly compete, the incumbent would have to create a completely separate, walled-off entity: a new brand, new facilities, and a new talent pool. At which point, they are simply building a direct competitor to themselves, begging the question: why not just let the insurgents take the low-margin market while you dominate the premium segment?

Verdict: This is a race against time. The incumbent’s inertia provides a crucial 3-5 year window of uncontested execution for the insurgents. If, within that window, they can build a defensible brand and lock in a critical mass of customers (especially with sticky subscription models), they can survive the inevitable counterattack. If they are still small and fragile when the giant finally wakes up, they will be crushed. The game is to build a moat before the incumbent realizes it’s at war.

Bear Case #6: Regulatory Capture (The Endgame Moat)

Thesis: This is the endgame. When an incumbent cannot win a war on the battlefield of the free market, it moves the conflict to a different venue: the state. This is the weaponization of bureaucracy. The goal is not to build a better product, but to lobby for a set of rules that makes the insurgent’s product illegal.

This is the most potent and cynical of the bear cases, because it has nothing to do with customers or quality. It is pure, brute-force political leverage. The incumbent argument will be cloaked in the language of “patient safety” and “quality standards,” but its true purpose will be to legislate the insurgents out of existence.

The Incumbent’s Political Playbook

The attacks will be surgical strikes on the insurgents’ core operational and economic advantages:

Weaponize ‘Quality’ Standards. Lobby for regulations that define a ‘real hospital’ in terms of the incumbent’s bloated cost structure. Mandate a minimum CAPEX-per-bed that just so happens to be impossible to meet with SuperHealth’s lean, asset-light model. Suddenly, SuperHealth’s innovation is rebranded as “substandard.”

Redefine ‘Scope of Practice’. Introduce rules that tie specific procedures to facility size. For example, “cardiac procedures can only be performed in 500+ bed hospitals.” This kills the insurgents’ smaller, distributed model and forces them to play the incumbent’s high-CAPEX game.

Strangle the Business Model in Red Tape. Argue that Even’s subscription is not ‘healthcare’ but ‘unregulated insurance.’ This triggers a decade-long review by the insurance regulator (IRDAI), effectively killing the model while it’s in the cradle.

Eliminate the Price Advantage. Lobby for price controls or standardized rate cards for all procedures. If SuperHealth is legally required to charge the same as Apollo, its primary competitive vector is gone.

This is not just a theoretical threat. This is the standard defense mechanism for entrenched industries in India, from taxis to telecom.

The Insurgent’s Asymmetric Warfare Doctrine

The insurgents cannot win a traditional lobbying war. They don’t have the war chest or the decades-long relationships. Their only path is to fight an asymmetric campaign.

Achieve Political Escape Velocity. The primary defense is speed. You must scale your customer base, and thus, your voting bloc faster than the incumbents can mobilize their lobbyists. It is much harder for a politician to ban a service that a million of their constituents already love. Your customer base is your political capital.

Build a Human Shield. Form alliances with patient advocacy groups and consumer rights organizations. Frame the public debate as “pro-patient innovators vs. anti-consumer cartels.” Make it politically toxic for any official to be seen siding with the expensive incumbents.

Weaponize the Truth. Use radical transparency on outcomes and pricing as a political tool. Make it blindingly obvious to the public and to regulators that your model delivers better results for less money. It is hard for a government to ban the thing that is provably working.

Exploit the Bugs in the System (Federalism). Healthcare regulation in India is a patchwork of state and central laws. If one state is captured by incumbents, you retreat and scale in a more favorable one. Use the federation’s complexity as a firewall against a monolithic regulatory attack.

Verdict: This is a real and potent risk. The outcome of this battle will be determined by a simple race: can the insurgents acquire a critical mass of patients before the incumbents can acquire a critical mass of politicians? If the insurgents can make their services essential to millions of middle-class voters, they win the lobbying war. If they are still a niche, marginal player when the political attack comes, they will be extinguished.

So, which bear case is most likely to kill the revolution?

My ranking:

Talent Problem (40% probability): Can’t find enough ethical doctors = Can’t scale = Model stays niche

Scaling Problem (25%): Grow too fast, quality collapses, brand destroyed

Trust Problem (15%): Patients never believe “cheap = good,” stick with expensive brands

Incumbent Counterattack (10%): Apollo wakes up, copies model, crushes insurgents with scale

Cherry-Picking Problem (5%): Exposed for only treating healthy patients, credibility destroyed

Regulatory Capture (5%): Government bans model under industry pressure

Combined probability that revolution fails: ~60-70%.

But here’s the thing: Even if SuperHealth and Even specifically fail, the model succeeds. Because they’ve proven it works. Others will copy. The doom loop is broken.

That’s what makes this a real revolution. It’s not about one company winning. It’s about one system replacing another.

Now let’s talk about how to actually build in this space.

Part VI: The Execution Playbook

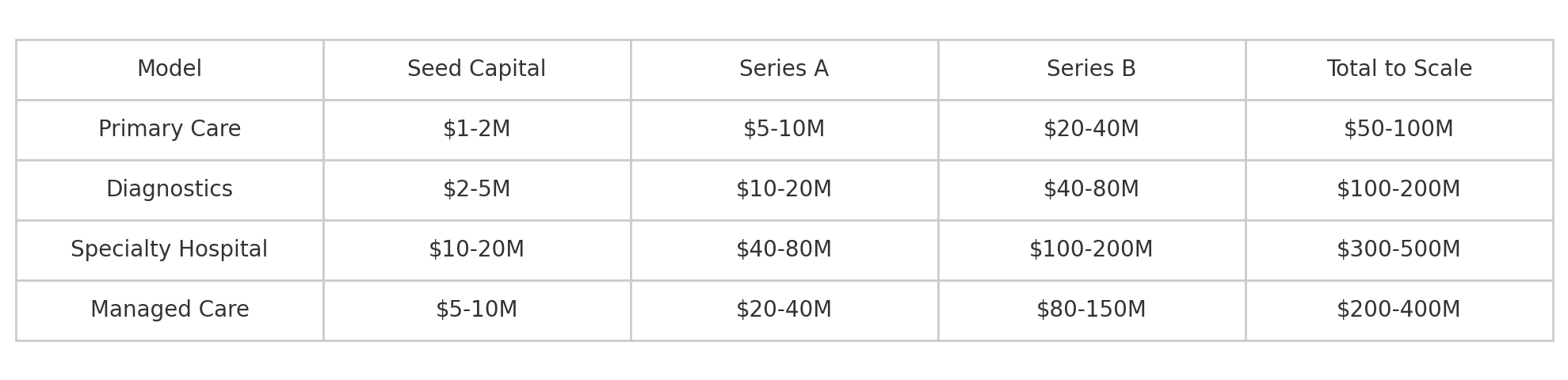

Okay, enough with the theory. This is the part of the memo where we move from analysis to allocation. You’re a founder or an investor, and you want to build a piece of this future. Where do you start?

Indian healthcare is a full-stack problem, but capital is deployed in tranches and companies are built in stages. You can’t build the entire Kaiser Permanente model on Day One. You need a wedge, an entry point into the value chain that allows you to build a defensible business before you earn the right to integrate vertically.

There are four primary entry vectors.

Vector 1: The Top-of-Funnel Play (Primary Care)

The Thesis: The structural flaw in Indian healthcare is the lack of a trusted, low-cost front door. 80% of health issues can be solved without a hospital, yet patients go straight to the most expensive node in the network. The opportunity is to build that front door and own the customer relationship at the top of the funnel.

The Stack: A hybrid model. A low-friction telemedicine platform for initial contact, paired with a distributed network of small, asset-light physical clinics for when you need to see a doctor in person.

The Economics: The prize isn’t the transactional margin on a single ₹500 consultation. That’s a low-margin, high-volume game. The prize is the pivot to a subscription model. Once you are the trusted primary care provider for 10,000 families, you can offer an “all-you-can-eat” primary care plan for a recurring fee, creating a predictable, high-LTV revenue stream.

The Moat: A trusted brand and a sticky, recurring relationship with the customer.

The Risk: This is a brutal, high-churn customer acquisition game. You are fighting against a deeply ingrained cultural habit of going straight to specialists.

Founder Archetype: The consumer tech operator. This is a CAC/LTV optimization game more than a medical problem. Think ex-Swiggy/Flipkart growth leads.

Vector 2: The “Intel Inside” Play (Diagnostics)

The Thesis: The diagnostic layer of the healthcare stack is a classic case of underutilized capital assets. Every hospital has its own lab, running at 30% capacity. This is an arbitrage waiting to happen. Standalone, centralized “factories” can process tests at a fraction of the cost.

The Stack: A hub-and-spoke logistics network. A large, centralized lab for processing, surrounded by a constellation of hyper-local collection centers and mobile phlebotomists.

The Economics: These are software-like gross margins. A blood test panel that costs ₹300 to process can be sold for ₹1,500. The entire business is a game of driving volume to maximize the utilization of the central factory.

The Moat: Economies of scale and logistical efficiency. Once you are the lowest-cost provider, you can become the B2B backend for everyone else: hospitals, insurers, and primary care clinics.

The Risk: This is a highly commoditized, price-sensitive market. You are competing with giants like Dr. Lal PathLabs and Thyrocare, who are engaged in a race to the bottom on price.

Founder Archetype: The supply chain and operations wizard. This is a problem for the ex-Delhivery/Amazon logistics manager who gets excited about route optimization and asset utilization.

Vector 3: The Full-Stack Wedge (Specialty Hospitals)

The Thesis: Instead of starting at the low-margin top of the funnel, you start with the hardest, most capital-intensive part: the hospital itself. But you re-engineer it from the ground up to be a lean, high-throughput machine. This is the SuperHealth playbook.

The Stack: Arbitrage distressed commercial real estate. Build smaller, 50-100 bed facilities. Convert every possible piece of CAPEX to OPEX (e.g., Equipment-as-a-Service). Focus on a narrow band of high-volume, predictable procedures.

The Economics: This isn’t a venture-scale business in its early days; it’s more of a private equity play. It requires significant upfront capital (₹35-70 crores per facility), but if executed correctly, it can achieve a 3–5-year payback period and generate stable, 15-20% EBITDA margins.

The Moat: Real, physical assets and deep operational excellence. This is the hardest model to copy.

The Risk: This is an execution-heavy, atoms-based business. It’s slow, capital-intensive, and carries significant talent risk.

Founder Archetype: The gray-haired operator. This is a game for the ex-hospital CEO or the real estate developer who knows how to get things built in the real world and can raise serious capital.

Vector 4: The God Mode Play (Managed Care)

The Thesis: This is the most ambitious and dangerous play. You ignore the existing value chain and go straight for the endgame: fixing the incentive problem at its source by becoming both the payer and the provider. This is the Even Healthcare playbook.

The Stack: You start as a “Virtual Integrated Provider,” using a subscription model and a software layer to manage care through partners. Then, as your subscriber base grows, you slowly, painfully, acquire the atoms, building your own clinics and hospitals to control the full stack.

The Economics: This is a pure underwriting game. Your profit is the spread between the premiums you collect and the cost of the care you deliver. The entire business is a bet that you can manage your Medical Loss Ratio (MLR) better than anyone else.

The Moat: A perfectly aligned system with powerful network effects and high switching costs. Once you reach scale, this is the most defensible model in all of healthcare.

The Risk: Existential. You are, in effect, an unregulated insurance company. A single, poorly managed risk pool can lead to an actuarial death spiral and bankruptcy. This requires the most capital and carries the highest risk of catastrophic failure.

Founder Archetype: The finance/insurance nerd with a stomach for existential risk. This is a game for the ex-actuary or hedge fund analyst who sees healthcare not as a service, but as a portfolio of risks to be managed.

Capital requirements by model:

The Talent Playbook

This is the primary constraint. Your elegant business model is a spreadsheet fantasy until you solve the human capital problem. Let me be explicit about how to think about this.

You are not just “hiring doctors.” You are executing a human capital arbitrage strategy. You cannot win a head-to-head cash compensation war against the FFS machine. Your entire playbook must be based on identifying and acquiring high-quality talent that is systematically mispriced or undervalued by the incumbent market.

Part 1: Acquiring the Clinical Assets (Doctors)

You are building a portfolio of clinical talent from three distinct, inefficiently priced market segments.

Segment 1: The Un-Corrupted Asset (New Graduates)

The Asset: Final-year residents from top medical colleges. They are clinically proficient but have not yet had their compensation expectations anchored to the FFS commission structure.

The Arbitrage: You are acquiring high-potential talent before the market has a chance to corrupt it. You are trading on their preference for mission and professional integrity over immediate cash maximization.

The Playbook: Target them aggressively on campus. Offer a clear alternative to the “sales” culture they are about to enter.

Segment 2: The Geographic Arbitrage (Tier 2/3 Returnees)

The Asset: Doctors trained in top-tier metro hospitals who have a non-financial preference to live in their hometowns.

The Arbitrage: You are acquiring a premium, metro-trained asset at a discounted, Tier 2 market price. Their “quality of life” preference is a market inefficiency you can exploit.

The Playbook: Build your early, non-metro hospitals specifically in cities known for exporting medical talent. You become the default “best option” for a high-quality doctor wanting to move home.

Segment 3: The System-Mismatch Asset (The Diaspora)

The Asset: Indian doctors working in salaried, evidence-based systems abroad (US, UK, Gulf) who want to return.

The Arbitrage: These are premium assets that are functionally incompatible with the Indian FFS market. You are the only bidder for this high-quality, ethically-trained talent pool.

The Playbook: Offer a “soft landing” package: a professional culture they recognize, assistance with navigating the Medical Council’s bureaucracy, and a solution to the “moral compromise” problem that keeps them abroad.

The Compensation Stack & The Pitch

Your offer is not just a salary; it’s a different kind of deal.

The Stack: A cash salary that is competitive but likely 10-20% below the all-in FFS equivalent, plus a meaningful grant of equity (0.1-0.5% for early, key hires) with a standard 4-year vest. The equity is the key to creating long-term incentive alignment, turning the agent into a principal.

The Pitch: You are offering an exit from a broken system and a chance to build the new one. The most powerful part of the pitch is not the mission, but the math: “Let us show you our unit economics. This is the financial model for why we don’t need you to be a salesman. We profit from efficiency and trust, not volume.”

Part 2: Acquiring the Operating System (Management)

You need a management team that is a hybrid of three distinct corporate DNAs.

The Frameworks (ex-McKinsey/Bain/BCG): You need the strategy consultants for their analytical rigor and their repeatable playbooks for scaling. They are the architects.

The Scaling Engine (ex-Ola/Swiggy/Flipkart): You need the startup veterans for their logistics-at-speed muscle memory and their experience in the brutal, chaotic reality of 0-to-1 execution in India. They are the builders.

The Domain Expertise (ex-Apollo/Fortis/Narayana): You need the industry insiders to de-risk the clinical operations and provide credibility. They are the domain experts who know where the bodies are buried.

The Ideal Founding Stack

The perfect founding team is a balanced portfolio of these archetypes:

CEO: A seasoned operator who has built something from nothing before and can integrate these disparate cultures.

Chief Medical Officer: A respected senior physician who can serve as the ultimate recruiting tool for other doctors.

CTO: A product and tech leader who understands how to build the technology that will allow the system to scale without collapsing.

CFO: A finance expert obsessed with the numbers, who ensures the revolutionary model remains profitable and doesn’t drift back toward the old ways.

The Regulatory Playbook

This is the non-clinical risk that keeps founders up at night. Regulation is not a checklist; it’s a game board. Here’s how to play it.

Playbook 1: The Bureaucratic Stack for Atoms (Opening a Hospital)

Before you treat a single patient, you must satisfy a multi-layered stack of bureaucratic approvals. This is a non-negotiable, friction-heavy process. The checklist of tollbooths includes:

The Clinical Establishments Act

The Municipal Corporation License

The Fire Department NOC

The Biomedical Waste Management Approval

The Pollution Control Board Clearance

...and several others.

The timeline for navigating this stack is a variable function of your local “consulting” budget.

Normal: 9-12 months.

Slow/Unlucky: 18-24 months.

Accelerated: 4-6 months.

This brings us to a non-negotiable line item in your Series A budget: the local “consultant.” This is typically a former government official who understands the system’s undocumented APIs. For a fee of ₹5-10 lakhs, they provide “friction reduction as a service.” This is not a bribe; it is the market rate for accelerating administrative processes.⁸

Playbook 2: The Great Regulatory Arbitrage (The Subscription Model)

This is where the real high-stakes game is played. The managed care model exists in a beautiful, terrifying regulatory grey area.

The Arbitrage: You are selling a product that, to the customer, feels like insurance, but to the regulator, is legally structured as a “pre-paid healthcare service membership.” This is a crucial distinction. It keeps you out of the clutches of the insurance regulator, IRDAI, whose approval process can take 3-5 years and requires a ₹100 crore capital reserve.